Multinational companies rely increasingly on cross-border employees. The legal and tax implications of employing workers from abroad are complex and it is well worth planning the tax and social security aspects in advance. Below we describe the three most common scenarios of cross-border employment in Hungary.

In our discussion of the most common scenarios we shall take the example of an engineer from Poland who is working in Hungary on a cross-border basis. As based on this example, we shall analyse the tax and social security consequences and options, shedding light also on some classic pitfalls. Although in our example the cross-border worker in Hungary is a Polish citizen, the considerations are similar for employees from other EU-countries such as Germany, Austria, Slovakia, etc.

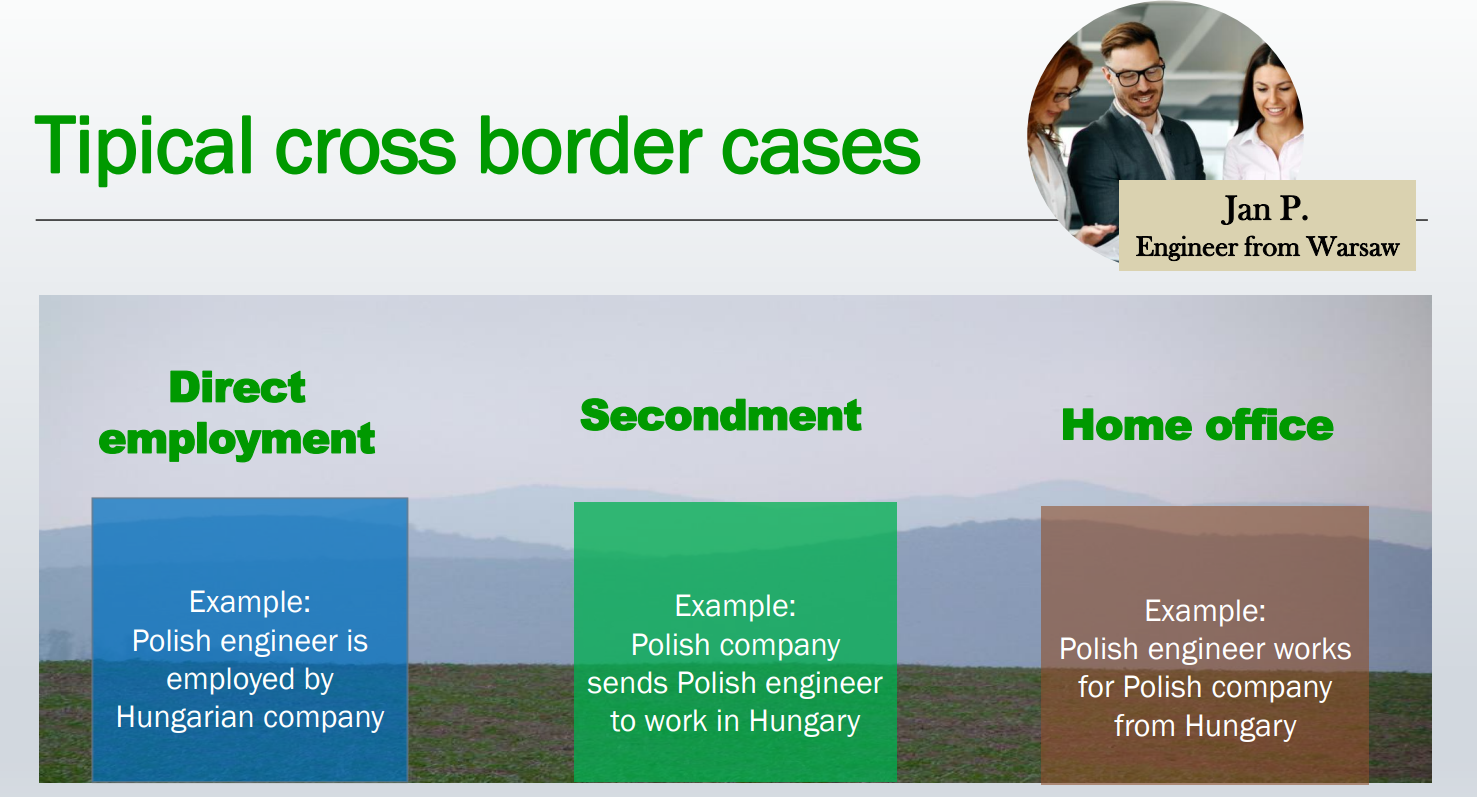

Summary: In this example the Polish engineer is employed by Hungarian company and he works in Hungary. Most typically, the all-over taxability of the engineer will be in Poland if the engineer remains a Polish tax resident. Personal income tax for work income will be due in Hungary, as well as social security.

Aspects to consider:

Two or more employers?

If the engineer normally works as an employee in two or more Member States, this can lead to an incorrect handling of social security by the employer. Employers often disregard the fact that in such cases the engineer will be subject to social security only in the Member State of residence (Poland). This exception from the general rule applies also in the case if a significant part of his activity is carried out in Poland, or if he is employed by different employers whose registered offices are located in other Member States than Poland.

Summary: In this example a Polish company sends a Polish engineer to work at a company in Hungary. Typically, personal income tax for work income will be due in Poland if the engineer spends 183 days or less in Hungary. If he spends more than 183 days in Hungary, then his work income will be taxed in Hungary, however his all-over taxability will be in Poland if the engineer is a Polish tax resident. Social security will be due in Poland.

Aspects to consider:

Summary: In this example the Polish engineer moves to Hungary permanently and carries out distance work for a Polish company from his home in Hungary. In most cases the all-over taxability of the engineer will be in Hungary including personal income tax for work income. Social security will also be due in Hungary.

Aspects to consider:

What about corporate income tax?

This question may seem out of place, however a person working at a home office in Hungary may create corporate income tax liability for the foreign employer. In our example, the Polish company may be deemed to have a “permanent establishment” in Hungary for corporate income tax purposes in a wide set of constellations, such as in the case of visiting and negotiating with customers.

In all cases of cross border employment, whether it is planned by a foreign or a Hungarian company, it necessary to analyse the tax and social security consequences on an individual basis for every employee in advance. The common scenarios described above have been based on an economic relationship between two EU Member States, namely Hungary and Poland. In this respect it is to be noted that the results of our general considerations would have been completely different if we had analysed examples involving a non-EU member country.

Note :This article is based on our presentation at the Hungarian-Polish Chamber of Commerce in February 2023.

We are dedicated to adding value to our clients’ businesses through understanding their objectives and supporting them in achieving their goals. With over 20 years of international experience and a strong focus on digitalization we provide full scale professional services at a single point of contact.

In our Case Studies we have described some examples of how we work for our clients and what benefits we have achieved for them.

A member firm of DFK International a worldwide association of independent accounting firms and business advisers